At EZInvest, we’re committed to providing fast, quality executions with the highest level of transparency.

tight spreads

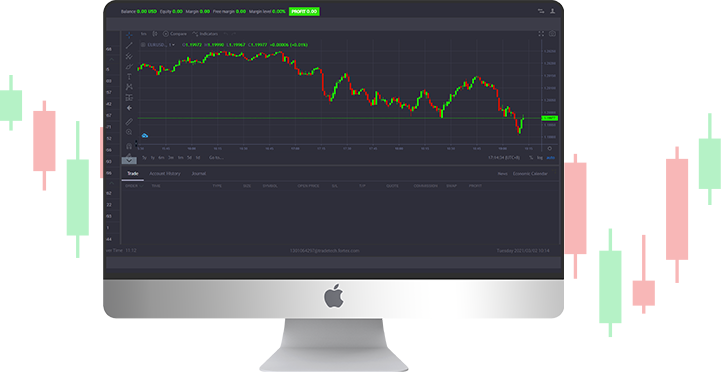

Our trading platform offers the largest selection of international currency pairs, all major indices, commodities, and CFD stocks on competitively tight spreads, helping you to lower your trading costs.

Hi-tech forex trading tools

Trade with confidence and benefit from our advanced tools and features for an excellent online trading experience.

Ultimate risk protection & security

With EZInvest you can trade smarter and minimize your risks by using our innovative technology and resourceful educational platform.

Play Video

About Us

Proven industry expertise

We work very hard to set the standard for professional trading in a crowded and relentless industry. We strongly believe that success relies on communication and the time we get to know our clients. At EZInvest, everything starts from the trading floor. We develop our services and products based on that first-hand knowledge that gives us a full understanding of what traders really need.

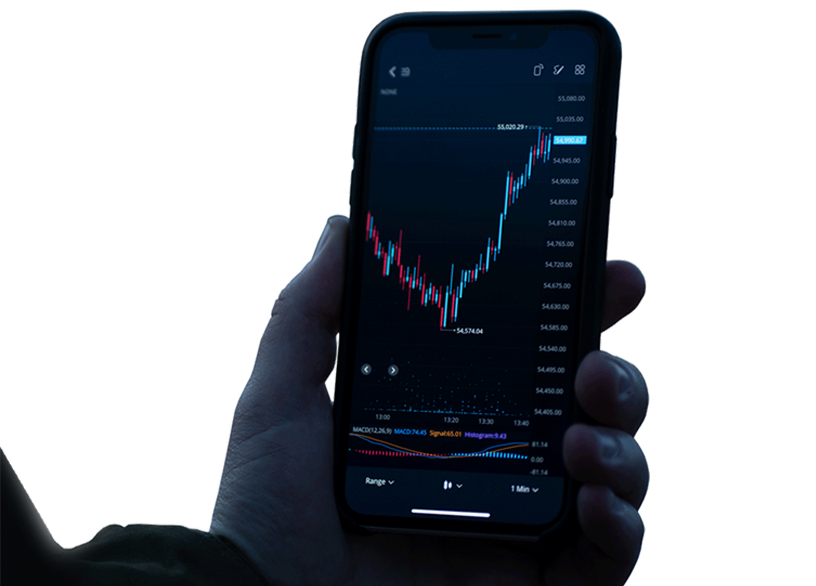

EZInvest Mobile is a fully-featured app for the trader on the go. With all of the charts and news that you’ll need to trade successfully, EZInvest Mobile offers an excellent trading experience and easier access to actively manage your portfolios, even when you are away from a desktop or laptop. The platform is compatible with Apple and Android devices. Enjoy & Experience one of the best mobile trading apps.

0+

Countries

0+

Trading Instruments

0+ years

Experience

IMPORTANT NOTICE

This page/website is not directed to EU clients and falls outside the European regulatory framework and is not in scope of(among others) the Markets in Financial Instruments Directive(MiFiD) II.

By continuing you acknowledge to view content provided by Sanus Financial Services which is authorised and regulated by the Financial Securities Conduct Authority (FSCA), South Africa and that the decision was made independently and at your own exclusive initiative and that no solicitation or recommendation has been made by Sanus Financial Services or any other entity within the group.

This website uses cookies to ensure you get the best experience on our website. By continuing to browse on this website, you accept the use of cookies for the above purposes.